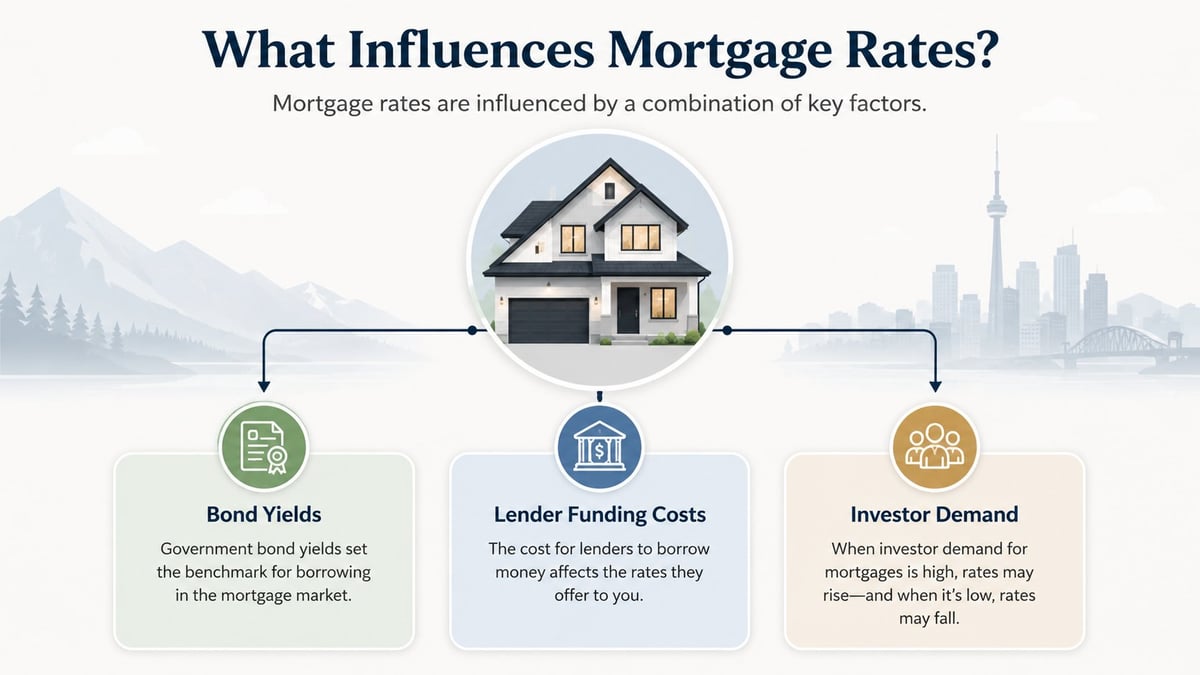

Why Mortgage Rates Move Even When the Bank of Canada Does Nothing

Most people assume mortgage rates move because the Bank of Canada says so. It makes sense. You hear about a Bank of Canada announcement in the news, then everyone starts asking whether mortgage rates are going up, going down, or staying the same.

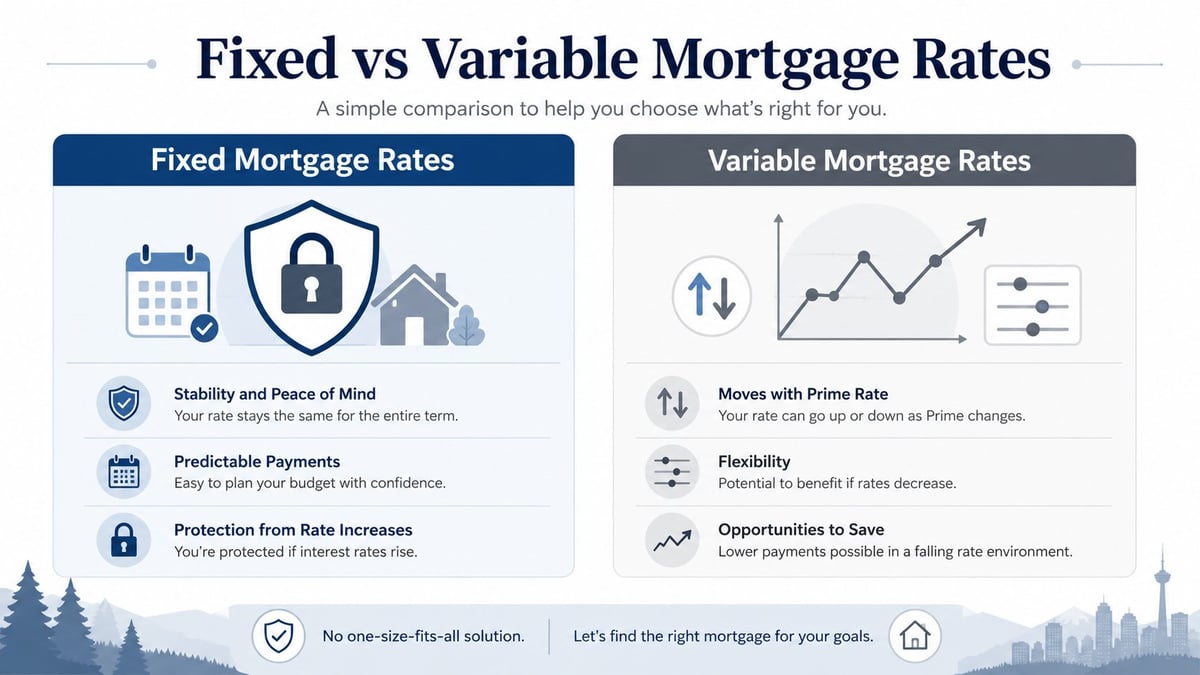

But here's the part many Canadians — and Manitoba homeowners — do not realize: The Bank of Canada is important, but it is not the whole story. In fact, one of the biggest reasons people feel confused about mortgage rates is because fixed mortgage rates and variable mortgage rates do not work the same way.

So when a Winnipeg homeowner asks us, "Why did rates move if the Bank of Canada did nothing?" — this is usually where the conversation starts. Mortgage rate pricing is more complicated than most people think. That does not mean you need to become an economist. But understanding the basics can help you make smarter decisions when buying, renewing, refinancing, or comparing mortgage options in Manitoba.